How COVID-19 Affected the US Economy: Statistics & Facts

The COVID-19 pandemic was much more than a public health crisis. As the virus migrated from China and began to spread to every country in the world, it had a far greater impact on the economy than mortality rates.

In the US, the pandemic paved the way for an unprecedented recession that threw tens of millions out of work while eroding incomes, benefits, and corporate profits.

The long-term economic consequences of this crisis are still being felt, as it's now clear that this was the greatest macro-shock to the world since the Great Depression.

Key Statistics to Consider - Editor’s Choice

- More than 100,000 small businesses shuttered across the US because of COVID.

- More than one in five US households were behind on rent in July 2020.

- In 2020, worldwide retail e-commerce sales amounted to $4.28 trillion.

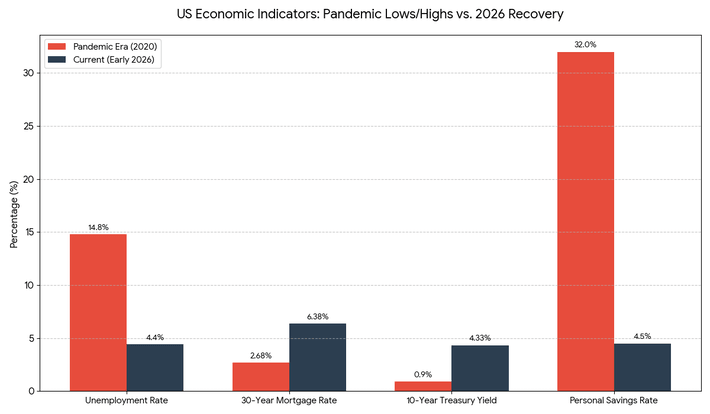

- The unemployment rate in the US hit 14.8% in April 2020.

- 3.3 million Americans filed for unemployment benefits in March 2020.

In Q2 of 2020, real gross domestic product declined at an annual rate of 32.9%.

(Bureau of Economic Analysis)

The onset of the recession in early 2020 had a devastating effect on the US economy. Data from the Bureau of Economic Analysis shows that the dramatic decline in GDP reflected a drop in everything from personal consumption expenditures and exports to government spending and private investment.

3.3 million Americans filed for unemployment benefits during the week ending March 21, 2020.

(The Washington Post)

The economic damage affected millions of Americans almost instantly, with the number of people filing for unemployment insurance soaring in a single week in March 2020.

The numbers only kept getting worse, and the following week 6.1 million people filed for the benefits.

This was an all-time high in US history. According to the US Department of Labor, the previous record was set on October 2, 1982, when more than 695,000 individuals filed for unemployment benefits.

The US unemployment rate hit 14.8% in April 2020.

(US Bureau of Labor Statistics)

Research and data compiled by the US Bureau of Labor Statistics reveal that April 2020 was the worst month on record since the Great Depression. Since then, the unemployment rate has gradually declined to 8.4% in August 2020 and 5.2% one year later.

Nevada and California had the highest unemployment rates in October 2021.

(US Bureau of Labor Statistics)

In October 2021, Nevada and California were the two states with the highest jobless rates in the country. They both had unemployment rates of 7.3%. During the same month, Arizona experienced the highest over-the-month unemployment rate decrease of -0.5 percentage points.

Meanwhile, Nebraska and Utah had the lowest unemployment rates - 1.9% and 2.2%, respectively.

Retail sales declined by 8.7% from February to March 2020.

(Brookings Institution)

As the government imposed lockdowns, many retailers experienced a decrease in demand, including clothing stores, restaurants, and gas stations. On the other hand, pharmacies, grocery stores, and e-commerce retailers experienced spikes in demand during the lockdowns.

More than 100,000 small businesses across the US shut down because of the coronavirus.

(US Chamber of Commerce)

A poll taken in early 2021 revealed that 86% of minority-owned small businesses were concerned about the economic impact of the COVID-19 pandemic and their business’s future.

That figure was slightly lower among non-minority-owned small businesses, with 72% saying they were worried about the future.

Although most small business owners (54%) believed that the availability of the coronavirus vaccine would make a difference, 59% didn’t expect a return to normalcy any time soon.

56% of small businesses preferred financial aid in the form of direct cash payments.

(US Chamber of Commerce)

Following the start of the pandemic, an exhaustive number of small companies turned to the federal government for financial aid to help them get through the crisis.

56% of those surveyed by the US Chamber of Commerce said they favored direct cash payments, while 30% said they would rather accept financial aid in the form of SBA disaster loans. Meanwhile, 21% of respondents think the temporary cancellation of business payroll taxes is the best option.

In May 2020, 48.7 million people reported they worked from home due to COVID-19.

(National Council on Compensation Insurance)

Prior to the pandemic, only 6% of the US workforce worked from home. The pandemic changed that, and the initial economic impact of COVID-19 pushed that figure to about 35%.

The US personal savings rate reached a record high in April 2020.

(Brookings Institution)

One of the immediate effects of the pandemic was a huge decline in aggregate spending, which naturally caused a significant increase in savings. Although the negative economic impact is obvious, the personal savings rate peaked at 34% in April 2020 due to greater federal transfer payments and lower spending.

More than one in five US households were behind on their rent in July 2020.

(Brookings Institution)

Many Americans were struggling with rent payments. An increase in federal payments to unemployed workers and households wasn’t enough to cover all their expenses and help them adequately manage their household finances.

The fixed rate for 30-year mortgages sank to record lows in December 2020.

(Freddie Mac)

The economic impact is also evident when looking at bank lending rates. According to data compiled by Freddie Mac, the fixed rate for 30-year mortgages dropped to 2.68% in December 2020.

That’s significantly lower when compared to December 2019 when mortgage rates were 3.72% and December 2018 when the rates were 4.64%.

However, rates rose sharply in subsequent years as the Federal Reserve battled inflation; by March 2026, the average 30-year fixed mortgage rate had climbed back to 6.38%.

The 10-year Treasury yield in the US fell below 1% in March 2020.

(US Department of Treasury)

Another clear example of the economic recession was the decline of the 10-year Treasury yield, which stood at 1.59% around mid-February. In the weeks that followed, it began its decline, and for the first time in 150 years, the 10-year Treasury yield dropped below 1% on March 5, 2020. Yields have since rebounded and moved higher due to shifting fiscal policies and inflation expectations, reaching 4.33% as of March 25, 2026.

The US core inflation rate reached a 40-year high of 6.6% in September 2022.

(Federal Reserve)

While the initial shock of the pandemic caused prices to stall, the subsequent reopening of the economy combined with severe supply chain disruptions and historic fiscal stimulus triggered the most significant inflationary period in decades. By early 2026, inflation has largely normalized, with the Consumer Price Index (CPI) rising 2.4% over the 12 months ending in February 2026.

The US labor force participation rate plummeted to 60.1% in April 2020.

(US Bureau of Labor Statistics)

This drop marked the lowest level of labor engagement since the 1970s, as millions of workers left the workforce due to health concerns, childcare needs, or early retirement. As of February 2026, the participation rate has partially recovered to 62.0%, though it remains below the pre-pandemic level of 63.3%, reflecting a lasting shift in the American labor pool.

The US national debt increased by approximately $6.5 trillion between 2020 and 2022.

(US Treasury)

To prevent a total economic collapse, the federal government launched massive relief programs, including the CARES Act and the American Rescue Plan. This led to a 50% increase in federal spending during the peak pandemic years.

Office vacancy rates in the US reached an all-time high of 20.1% in 2024.

(Moody’s Analytics)

The shift to remote and hybrid work models proved to be one of the most permanent economic legacies of COVID-19. Before the pandemic, office vacancies typically hovered around 12%.

Sources

I have always thought of myself as a writer, but I began my career as a data operator with a large fintech firm. This position proved invaluable for learning how banks and other financial institutions operate. Daily correspondence with banking experts gave me insight into the systems and policies that power the economy. When I got the chance to translate my experience into words, I gladly joined the smart, enthusiastic Fortunly team.