Articles

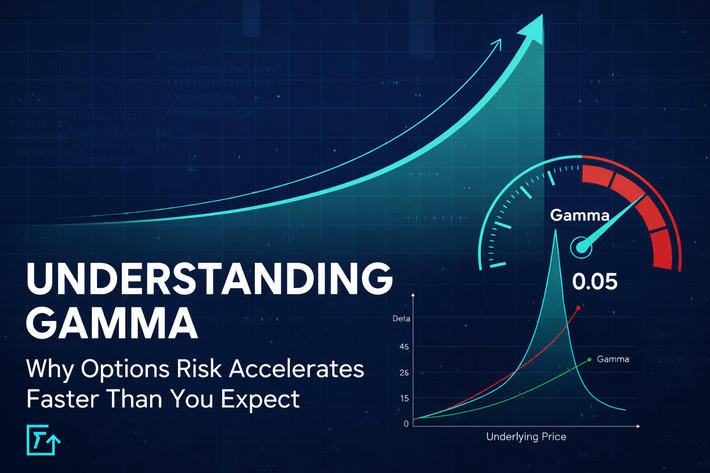

Gamma determines the rate of change in Delta for every $1 move in the stock.

February 02, 2026

Read Article